THE DOOLEY ANALOGY

- 1945: condition of the stock of productive capital [Colditz] [Danzig] [Japan].

- China & Cultural Revolution [VIDEO]

Other:

- US Debt clock.

{kind=link}

{kind=link}

{kind=link}

Tuesday, April 19, 2011

DEBATE: WILL CHINA GRADUATE FROM AN EXPORTING PERIPHERY TO A CENTER OF INNOVATION AND GROWTH?

Is this a relevant debate? How would if affect the world economy and international relations?

__________________

Documents & ideas: wages, consumption

[1] China’s currency regime: a tax on consumption? “The currency regime is a tax on consumption, which accounts for a mere 36 per cent of gross domestic product and represents a considerable subsidy to exports” (George Magnus, UBS economist: “A stronger yuan is just a start for China”, Financial Times, March 23, 2010).

[3] Strike at Honda factories in Guandong, May-June 2010 [VIDEO]. “The killer fact was that the share of wages and salaries in GDP dropped to a mere 37 per cent of GDP in 2005, from 57 per cent in 1983, and remained static since then. Low pay, long working hours and poor working conditions for millions of workers are triggering conflicts and mass incidents, which pose a grave challenge to social stability. The remarkable low share of wages and salaries in GDP makes China the most ‘capitalist’ large economy in history. Until this is reversed, the much-desired shift to a consumption-driven economy cannot occur. Over time, a better balanced economy with higher wages and standards of living, will emerge. The rise in pay announced by Foxconn and Honda looks like an entirely natural consequence of the country’s development and of the operation of labor markets, such as they are allowed to function. Productivity has risen over the decades, partly because of more capital per employee but also as a result of higher skill among workers.” (“Chinese workers are now in open revolt”, Financial Times, June 4, 2010; “Why China’s pay unrest is healthy”, June 12, 2010).

Documents & ideas: the role of education

[1] The PISA tests. [2009 RESULTS]. Many people in the West were shocked by the results! Shanghai comes on top. (Don’t even look at Argentina).

[2] Amy Chua. Battle Hymn of the Tiger Mother. New York: Penguin, 2011 [VIDEO] [VIDEO] [Interview] (*).

Documents & ideas: the rule of law and the cost of capital (back to Montesquieu and Smith!)

_________________

Concluding remarks. Will China ‘graduate’ from periphery to center? Ai Weiwei & Francis Fukuyama

. Why is there no ‘Chinese De Gaulle’? (The 1968 dollar crisis and the ‘addiction’ to exports; the invasion of Czechoslovakia and the flight-to-safety that undoes De Gaulle).

Francis Fukuyama: (1) “Can China push back the frontiers of science and technology without Western-style property rights or personal freedom?; (2) The welfare state: no taxation without representation, a key element of political accountability; (3) Connectivity. “Darwinian” evolution takes place at the level of human institutions! Given the connected nature of today’s world, that process of evolution may take place a lot faster than in the past. And that’s where Ai Weiwei joins Fukuyama: social network sites are very active in mobilizing support for the artist. See @Change; #freeaiweiwei; #aiweiwei; Lee Ambrozi. Ai Weiwei’s blog. Writing, Interviews and Digital Rants by Ai Weiwei. MIT Press, 2011; “Chinese Hackers Attack Change.org Platform in Reaction to Ai Weiwei Campaign”.

Is this a relevant debate? How would if affect the world economy and international relations?

__________________

Documents & ideas: wages, consumption

[1] China’s currency regime: a tax on consumption? “The currency regime is a tax on consumption, which accounts for a mere 36 per cent of gross domestic product and represents a considerable subsidy to exports” (George Magnus, UBS economist: “A stronger yuan is just a start for China”, Financial Times, March 23, 2010).

[2] Suicides at Foxconn. Foxconn is the world’s largest electronics manufacturer; it employs 540.000 workers. It has been described as “the workshop of the world” and as “the backbone of world’s electronic manufacturing system. Its clients include Apple, Dell, HP, Nokia. Twelve workers committed suicide in early 2005 in Shenzhen. Then the company announced a 20% pay rise, from an average of €113/month. Yang Lixiong of Renmin Univeristy in Beijing: “Our country is on a race to the botton because our only advantage is cheap labor, and therefore our development is built on a mountain of sweatshops”. (Kathrin Hille: “Showing the strain”, Financial Times, May 29, 2010) [VIDEO].

[3] Strike at Honda factories in Guandong, May-June 2010 [VIDEO]. “The killer fact was that the share of wages and salaries in GDP dropped to a mere 37 per cent of GDP in 2005, from 57 per cent in 1983, and remained static since then. Low pay, long working hours and poor working conditions for millions of workers are triggering conflicts and mass incidents, which pose a grave challenge to social stability. The remarkable low share of wages and salaries in GDP makes China the most ‘capitalist’ large economy in history. Until this is reversed, the much-desired shift to a consumption-driven economy cannot occur. Over time, a better balanced economy with higher wages and standards of living, will emerge. The rise in pay announced by Foxconn and Honda looks like an entirely natural consequence of the country’s development and of the operation of labor markets, such as they are allowed to function. Productivity has risen over the decades, partly because of more capital per employee but also as a result of higher skill among workers.” (“Chinese workers are now in open revolt”, Financial Times, June 4, 2010; “Why China’s pay unrest is healthy”, June 12, 2010).

[3] Institutional aspects: the welfare state. How does the one-child policy affect saving-and consumption patterns? [A student in Santo Domingo] [The Sichuan earthquake] From UBS economist George Magnus: “Imbalances will not go away so long as China has an entrenched savings excess – the product of an unreformed rural sector, inmature social security and financial systems, and the one-child-policy” (“We need more from China than a flexible yuan”, Financial Times, 22 June 2010)

___________________Documents & ideas: the role of education

[1] The PISA tests. [2009 RESULTS]. Many people in the West were shocked by the results! Shanghai comes on top. (Don’t even look at Argentina).

[2] Amy Chua. Battle Hymn of the Tiger Mother. New York: Penguin, 2011 [VIDEO] [VIDEO] [Interview] (*).

(*) Dr. Chua is also the author of Day of Empire: How Hyperpowers Rise to Global Dominance--and Why They Fall. New York: Anchor, 2009.

[3] Google & China. “Google has accused the Chinese authorities of disrupting its e-mail service inside the country, adding a new twist to the standoff over censorship that has bedeviled the US company’s attempts to push into the world’s most populous internet market” (Richard Waters: “Google claims Beijing is disrupting e-mail service”, Financial Times, March 22, 2011). [DEBATE: Knowledge & freedom].

[4] Education and economic performance. The brain drain problem. Does France subsidy the US? South Korea vs. the Philippines. Iranian doctors in medicine in Canada. Venezuelan oil engineers in the US.

[5] Education and economic performance. The silence of Mr. Fukuyama.

___________________Documents & ideas: the rule of law and the cost of capital (back to Montesquieu and Smith!)

[1] Patti Waldmeir: “Things improve, but judiciary still lacks independence”, Financial Times. Waldmeir quotes Australian lawyer Doug Clark: “The perception that the legal playing field is not level is a larger impediment to Shanghai's ambition to become a global financial centre by 2020 than any number of potholed streets or immature trading mechanisms. Without an independent legal system that resolves disputes fairly no one will bring real money to Shanghai. No one is going to park $1bn in Shanghai to pick up a bit of margin unless they have confidence that they can call a judge at 2am and get an injunction against behaviour that could damage them ... In a country without an independent judiciary, laws are only as good as the politicians allow them to be enforced. Being a global financial center means your neighbour puts money in your pocket. At the moment, the confidence is not there for that”.

This brings us back to old, yet powerful ideas of Montesquieu and Adam Smith. No judicial independence, no credit. No credit, no entrepreneurship. No entrepreneurship, no prosperity.

[2] Ai Weiwei. [DOCUMENT: “Who is afraid of Ai Weiwei?”]

_________________

Concluding remarks. Will China ‘graduate’ from periphery to center? Ai Weiwei & Francis Fukuyama

. Why is there no ‘Chinese De Gaulle’? (The 1968 dollar crisis and the ‘addiction’ to exports; the invasion of Czechoslovakia and the flight-to-safety that undoes De Gaulle).

. Ai Weiwei’s diagnosis : CHINA IS A COLOURFUL COUNTRY AND THERE IS A LOT OF FREEDOM. YET THE LACK OF AN INDEPENDENT JUDICIARY AND STATE LIMITS ON FREE SPEECH ARE FATAL FLAWS. CHINA IS LIKE A RUNNER SPRINTING VERY FAST BUT WITH A HEART CONDITION (“Lunch with the FT: Ai Weiwei”, Financial Times, April 23, 2010) [info]. If he is accused of economic or sexual crimes, that would be the best illustration of the lack of judicial independence.

Francis Fukuyama: (1) “Can China push back the frontiers of science and technology without Western-style property rights or personal freedom?; (2) The welfare state: no taxation without representation, a key element of political accountability; (3) Connectivity. “Darwinian” evolution takes place at the level of human institutions! Given the connected nature of today’s world, that process of evolution may take place a lot faster than in the past. And that’s where Ai Weiwei joins Fukuyama: social network sites are very active in mobilizing support for the artist. See @Change; #freeaiweiwei; #aiweiwei; Lee Ambrozi. Ai Weiwei’s blog. Writing, Interviews and Digital Rants by Ai Weiwei. MIT Press, 2011; “Chinese Hackers Attack Change.org Platform in Reaction to Ai Weiwei Campaign”.

Tuesday, April 12, 2011

SOME LINKS FOR SESSION 3, APRIL 13

- World Bank Governance Indicators. The WB's Worldwide Governace Indicators (WGI). Click on Access Governance Indicators, and pick a country.

- Fraser Institute's Economic Freedom of the World report. See the Country Data Tables.

- World Economic Forum's chart on judicial independence.

- Freedom House's Freedom of the Press Survey.

- Ai Weiwei. David Piling: “Lunch with the FT: Ai Weiwei”, Financial Times, April 23, 2010. From one of his tweets: "No outdoor sports can be more elegant than throwing stones at autocracy; no melees can be more exciting than those in cyberspace". See his work at Haus der Kunst in Munich [see]; he also consulted with Swiss architects Herzog & de Meuron for the design of the Olympic Stadion in Beijing (The Nest). Says Ai Weiwei:

CHINA IS A COLOURFUL COUNTRY AND THERE IS A LOT OF FREEDOM. YET THE LACK OF AN INDEPENDENT JUDICIARY AND STATE LIMITS ON FREE SPEECH ARE FATAL FLAWS. CHINA IS LIKE A RUNNER SPRINTING VERY FAST BUT WITH A HEART CONDITION.

[DOCUMENT: “Who is afraid of Ai Weiwei?”]

See also Edward MacMillan-Scott: “Ai Weiwei's arrest is part of China's new crackdown”, The Guardian.

- Ambrogio Lorenzetti. Video; Justice; Good government in the countryside; Tyranny.

- Francis Fukuyama. The Origins of Political Order, Vol. 1 (New York: Farrar, Strauss & Giroux, 2011) [web] [Nicholas Wade: "From ‘End of History’ Author, a Look at the Beginning and Middle", The New York Times] [video].

- World Bank Governance Indicators. The WB's Worldwide Governace Indicators (WGI). Click on Access Governance Indicators, and pick a country.

- Fraser Institute's Economic Freedom of the World report. See the Country Data Tables.

- World Economic Forum's chart on judicial independence.

- Freedom House's Freedom of the Press Survey.

- Ai Weiwei. David Piling: “Lunch with the FT: Ai Weiwei”, Financial Times, April 23, 2010. From one of his tweets: "No outdoor sports can be more elegant than throwing stones at autocracy; no melees can be more exciting than those in cyberspace". See his work at Haus der Kunst in Munich [see]; he also consulted with Swiss architects Herzog & de Meuron for the design of the Olympic Stadion in Beijing (The Nest). Says Ai Weiwei:

{kind=link}

CHINA IS A COLOURFUL COUNTRY AND THERE IS A LOT OF FREEDOM. YET THE LACK OF AN INDEPENDENT JUDICIARY AND STATE LIMITS ON FREE SPEECH ARE FATAL FLAWS. CHINA IS LIKE A RUNNER SPRINTING VERY FAST BUT WITH A HEART CONDITION.

[DOCUMENT: “Who is afraid of Ai Weiwei?”]

See also Edward MacMillan-Scott: “Ai Weiwei's arrest is part of China's new crackdown”, The Guardian.

- Ambrogio Lorenzetti. Video; Justice; Good government in the countryside; Tyranny.

{kind=link}

{kind=link}

- Francis Fukuyama. The Origins of Political Order, Vol. 1 (New York: Farrar, Strauss & Giroux, 2011) [web] [Nicholas Wade: "From ‘End of History’ Author, a Look at the Beginning and Middle", The New York Times] [video].

Tuesday, April 5, 2011

The Political Economy of Credit Markets – Putting politics back into the credit market!

The Political Economy of Credit Markets – Putting politics back into the credit market!* * *

International Political Economy - Agustin Mackinlay

_________________

The Problem…

We now reach a key point in our IPE program! Normally at this stage, instructors would introduce central banks, short-term interest rates, monetary policy. Equipped with these tools, they would perhaps tackle the 2008 financial crisis. But I refuse to take that road. It deviates from one of the key points in today’s IPE scenario: the rise of new Great Powers (BRICs and others). What I have in mind is an altogether more ambitious project: LET US REINTRODUCE POLITICS INTO THE CREDIT MARKET!

What I call the Political Economy of the Credit Market is part of a research project of mine; it is the result of many years of reading and … traveling! South America, Mexico, Central America, Vietnam, The Philippines, Russia, Continental Europe, London, New York, San Francisco, New Zealand and —crucially— The Netherlands. The Political Economy of the Credit Market will help us better understand what David Landes called The Wealth and Poverty of Nations. Why Some are so Rich and Some so Poor (New York: 1998, W.W. Norton).

Consider column [6] in the table. The Netherlands have the largest bond market in terms of GDP (229%), while Peru ranks the lowest (12%). What is a bond? It is a CONTRACTUAL OBLIGATION that specifies the name of the issuer, the size of the issue, the way (and the dates) interest rate and principal payments are to be paid. Companies and governments issue bonds to finance innovation and public spending. What is GDP? The value of all goods and services produced in a given year.

If the Netherlands’ GDP amounts to $650 billion, then the size of its bond market is about … $1488.5 billion. (Peru numbers: $250 bn GDP; $30 bn size of bond market). No wonder the Netherlands are considered one of the wealthiest countries on the planet!

[DIAGRAM: Chart the supply of loanable resources in The Netherlands and Peru]

No credit, no entrepreneurship, no innovation; no credit, no infrastructure projects, no development. No credit, no jobs! No credit, no power on the international scene!

Some ideas…

Let me share some thoughts, numbers and books & articles with you on the political economy of the credit markets. Here are some papers that attempt to quantify the link between governance indicators and the size of the credit markets.

[NOT required reading!] Philip Keefer: “Beyond legal origin and checks and balances: Political credibility, citizen information and financial sector development”, in Stephen Haber, Douglass C. North & Barry Weingast (eds). Political Institutions and Financial Development (Stanford University Press, 2008) [available at Google Books]

[NOT required reading!] John D. Burger & Francis E. Warnock: “Local Currency Bond Markets”, IMF Staff Papers, Vol. 53, 2006 (only pp. 141-142).

[NOT required reading!] Kee-Hong Bae & Vidhan Goyal: “Creditor Rights, Enforcement, and Bank Loans”, The Journal of Finance, Volume 64, Issue 2, 823–860, April 2009. ABSTRACT: “We examine whether differences in legal protection affect the size, maturity, and interest rate spread on loans to borrowers in 48 countries. Results show that banks respond to poor enforceability of contracts by reducing loan amounts, shortening loan maturities, and increasing loan spreads. These effects are both statistically significant and economically large. While stronger creditor rights reduce spreads, they do not seem to matter for loan size and maturity. Overall, we show that variation in enforceability of contracts matters a great deal more to how loans are structured and how they are priced”.

These papers tend to present econometric models; while valuable, they provide little information about cause-and-effect relations. My first approach was to tackle the issue from the historical point of view. It turns out that the Netherlands has been at the forefront of financial development since the … XVIIth century! It has always been a low-interest rate country.

[NOT required reading!] “In 1665 Sir George Downing, writing in England, pointed out that it was possible for merchants to borrow in Amsterdam at 4 per cent or even 3 per cent, and in 1688 Sir Josiah Child took 3 per cent as normal. Rates of 2 ½ per cent are even mentioned.” [From: Peter Spufford: “Access to credit and capital in the commercial centres of Europe”, in Karel Davids & Jan Lucassen, eds. A Miracle Mirrored. The Dutch Republic in European Perspective. Cambridge University Press, 1995, p. 305].

Now from the man himself. Sir Josiah Child and the “miracle” of Dutch interest rates (*):

[NOT required reading!] “The prodigious increase of the Netherlands in their domestic and foreign trade, riches and multitude of shipping, is the envy of the present, and may be the wonder of all future generations: and yet the means whereby they have thus advanced themselves are sufficiently obvious, and in a great measure imitable by most other nations, but more easily by us of this Kingdom of England.

The Dutch trade honestly, and methodically; they wisely teach their children arithmetic and book-keeping in the schools; they encourage inventions and new manufactures; they have set up banks; they have introduced laws under which trade disputes are quickly settled. Most miraculous of all, however, they have succeeded in reducing their rate of interest to three per cent. (as against six per cent. in England). This, in my poor opinion, is the causa causans of all the other causes of riches in that people: and if the interest of money were with us reduced to the same rate as it is with them, it would in a short time render us as rich and as considerable in trade as they are now.

(*) Sir Josiah Child. Brief Observations concerning Trade and the interest of Money (1665), in Charles Wilson. Holland and Britain. London: Collins, no date, pp. 22-23.

___________

But how do we account for the Dutch miracle from the credit market perspective? This quote from Dutch historian Ernst Kossmann contains an important clue. In 1675, William III had accepted the sovereignty over Gelderland (from where William had successfully ejected the French army). The States of Gelderland awarded him the title of Duque. Scandal!

[NOT required reading!] “Even his most unconditional supporters were alarmed; the fury was so great that William felt obliged to refuse the award. In Zeeland he was told by his own supporters that an arbitrary government, the unavoidable consequence of a one-headed system of government –the standard argument of Dutch republicans– would undermine confidence in the commercial and financial institutions of the Republic, which in turn would destroy Dutch prosperity.” [From: E. H. Kossmann. Geschiedenis is als een olifant. Amsterdam: Bert Bakker, 2005, p. 166].

In other words, XVIIth century Dutchmen seemed to have detected a relationship between the form of government and financial stability.

The Montesquieu-Smith Approach: Montesquieu

French author Montesquieu (1689-1755) is mostly known for his analysis of the English Constitution in The Spirit of the Laws (1748). But he was an economist too. John Maynard Keynes, in the foreword to the French edition of his General Theory, calls Montesquieu “the greatest French economist of all times”. Montesquieu establishes a link between the type of government, interest rates and the size of the credit markets. Remember that whenever one lends money (or any other real resource), he / she is temporarily ceding the possession of those resources. Throughout the life of the loan –which is a contractual obligation– the lender runs the risk of not being repaid. The more politicized the courts of justice, the higher the risk! (examples a bit later on.)

[Montesquieu - REQUIRED READING!] “Poverty and the uncertainty of fortunes naturalizes usury in despotic states, as each one increases the price of his silver in proportion to the peril involved in lending it. Therefore, destitution is omnipresent in these unhappy countries; there everything is taken away, including the recourse to borrowing (Book V, chapter 15). In moderate states, it is entirely different. Confiscations would render the ownership of goods uncertain; they would despoil innocent children … In these countries of the East, most men have nothing that is secure; there is almost no relation between the present possession of a sum and the expectation of having it back after lending it; therefore, usury increases in proportion to the peril of insolvency (Book XX, chapter 19). These continual changes [in legislation regarding loans in the Roman republic], both by laws and by plebiscites, naturalized usury in Rome, as the creditors who saw in the people their debtor, their legislator, and their judge no longer had trust in contracts” [From: Montesquieu. The Spirit of the Laws, Book XX, chapter 21].

The Montesquieu hypothesis: DESPOTIC GOVERNMENT = UNCERTAINTY OVER THE PERFORMANCE OF CONTRACTS = UNSTALBE PROPERTY RIGHTS = SMALL SIZE OF CREDIT MARKETS = POVERTY & USURY!

[DIAGRAM]. The Montesquieu hypothesis. In despotic governments, the supply of loanable resources is much lower than in moderate regimes. REMEMBER THAT WHEN ONE LENDS RESOURCES, ONCE CEDES (ALBEIT TEMPORARILY) THE POSSESSION OF THOSE RESOURCES TO A THIRD PARTY.

And what is the defining feature of a despotic government in Montesquieu’s analysis? An excessive concentration of political power — most notably the lack of JUDICIAL INDEPENDENCE. Thus we can conclude: no judicial independence, no security about the performance of contracts, no stability in property rights, and hence a contraction in the supply of loanable resources in credit markets. Whenever the judiciary depends on the executive power, HIGH INTEREST RATES and poverty will prevail. Confidence will vanish; corruption will prevail.

The Montesquieu-Smith Approach: Ferdinando Galiani

Galiani on interest rates. A great quote from Ferdinando Galiani (1727-1787), a follower of Montesquieu. Galiani writes about interest rates in Della Moneta (1751). He argues that interest rates fell across Europe not because of the abundance of money, but thanks to the effects of moderate government (la dolcezza del governo). Galiani clearly reasons in terms of the supply of loanable resources. Note the comment on the abundance of credit and its impact on poverty. Sadly, I cannot provide a decent translation!

[NOT Required Reading!] Per render bassi gl'interessi secondo l'esposto di sopra basta evitare il monipolio del danaro, e assicurare la restituzione. Perciò non è stata la sola abbondanza de' metalli preziosi che ha sbassate e quasi estinte le usure da due secoli in qua; ma principalmente la dolcezza del governo quasi in ogni regno goduta. Sieno le liti brevi, la giustizia certa, molta industria ne' popoli, e parsimonia, e saranno tutti i ricchi inclinati a prestare. Là dove è folla di offerenti, non possono esser dure le condizioni dell'offerta. Così saranno i poveri trattati senza crudeltà.

Brilliant! Genius! And he was only 24 when he wrote this! Galiani explains the drop in interest rates in Europe from the Middle Ages to about 1750. He rejects a purely monetary explanation; rather, he adopts a political economy framework: it was not the abundance of money which led to lower interest rates. IT WAS MODERATE GOVERNMENT AND A SOUND JUDICIAL SYSTEM THAT DID IT!

The Montesquieu-Smith Approach: Adam Smith

Scottish philosopher and economist Adam Smith was well aware of Montesquieu’s work. In his 1776 major book, An Inquiry into the ealth of Nations (1776), he further elaborates on the link between interest rates and judicial independence.

[Adam Smith (1) - REQUIRED READING!]. When the law does not enforce the performance of contracts, it puts all borrowers nearly upon the same footing with bankrupts or people of doubtful credit in better regulated countries. The uncertainty of recovering his money makes the lender exact the same usurious interest which is usually required from bankrupts. Among the barbarous nations who over-ran the western provinces of the Roman empire, the performance of contracts was left for many ages to the faith of the contracting parties. The courts of justice of their kings seldom intermeddled in it. The high rate of interest which took place in those ancient times may perhaps be partly accounted from this cause. In Bengal, money is frequently lent to farmers at forty, fifty and sixty per cent and the succeeding crop is mortgaged for the payment. Interest is raised by defective enforcement of contracts. (Wealth of Nations, Book I, chapter 9).

[Adam Smith (2) - REQUIRED READING!] When the judicial is united to the executive power, it is scarce possible that justice should not frequently be sacrificed to, what is vulgarly called, politics. But upon the impartial administration of justice depends the liberty of every individual, the sense which he has of his own security. In order to make every individual feel himself perfectly secure in the possession of every right which belongs to him, it is not only necessary that the judicial should be separated from the executive power, but that it should be rendered as much as possible independent of that power (Wealth of Nations, Book V, chapter 1).

[Adam Smith (3) - Not required reading!] This Separation of the province of distributing Justice between man and man from that of conducting publick affairs and leading Armies is the great advantage which modern times have over antient, and the foundation of that greater Security which we now enjoy both with regard to Liberty, property and Life. It is evident that in quoting præcedents the more directly they agree with the case in hand in all its circumstances it will be so much the better. (Lectures On Rhetoric and Belles Lettres, 1762)

Many points can be made about these excellent passages. Any ideas? My takeaway: (1) The size of the supply of loanable resources depends on the security of property and on trust on the performance of contracts; (2) Trust in the performance of contracts depends on the existence of a well-functioning judiciary; (3) Whenever those conditions are not met, citizens pay an “extra-tax” in the form of higher interest rates! (“The uncertainty of recovering his money makes the lender exact the same usurious interest which is usually required from bankrupts”); (4) Judicial independence is … modernity!

The Montesquieu-Smith Approach: Jacques Necker

A former minister of finance under Louis XVI, Jacques Necker is a fierce opponent of the Napoleon regime. According to Necker, the regime —which rests on an unprecedented concentration of political power — is unsustainable because it leads to much too high interest rates. See Necker’s Dernières vues de politique et de finance (1802):

[NOT Required Reading!] La plenitude du credit [est] incompatible avec l’existence d’un pouvoir sans balance (p. 382). While England pays about 3% on her debt, the lack of confidence in the French regime means that the country pays as much as 9%.

Judicial Independence: the key ingredients

[1] Judges’ nomination process

[2] Tenure on good behavior

[3] Precedents as a source of law

[4] Due process of law

[5] Salaries and budget issues

All of this sounds a bit tedious. So let’s consider a number of recent and historical examples.

Russia

* * *

The Hermitage Capital story. In 2007, 230 million were stolen from Russian tax authorities by a gang of murderers who obtained “sham” judgments from judges in Moscow, St. Petersburg and Kazan. The fraud involved three subsidiaries of Hermitage that had paid taxes worth $230m. Soon after the police raid, these companies were fraudulently re-registered under new owners, who applied for, and immediately received, a tax rebate of $230m

[DOCUMENT: Hermitage Capital Video]

Lawyer Sergei Magnitsky found dead in his cell. Says Hermitage Capital’s Bill Browder: “Now, you have a bunch of law enforcement people who are essentially organised criminals with unlimited power to ruin lives, take property and do whatever they like and that's far worse than I have ever seen in Russia before. Russia is essentially a criminal state now.” From an unnamed senior banker in Mosow: “Russia's judicial system is totally compromised. It is strangling entrepreneurship. What happened is a clear impediment for investments coming in, not just for foreign investment but even for local ones”. (Catherine Belton: "Questions remain about Russia tax fraud", Financial Times). Note the point made by the senior banker: THE JUDICIAL SYSTEM STRANGLES ENTREPRENEURSHIP!!! Very much in line with Montesquieu-Smith.

[DOCUMENT: “Justice for Sergei”. See also The Economist: “Sergei Magnitsky one year on”, November 2010]

[QUESTION: WHAT CAN WE EXPECT FROM THOSE WHO SUPPLY LOANABLE RESOURCES IN THE RUSSIAN CREDIT MARKET]

On Russia’s “legal nihilism”. Olga Kudeshkina: “Tackling Russia’s Legal Nihilism”, OD Russia, 11 March 2010: “The powers of a judge who does not agree to carry out requests may be prematurely terminated. In such a situation the conscientious judge finds himself open to pressure from within the judicial system and has no chance of defending his or her own rights. As a result, fewer conscientious judges remain in service; their colleagues fear to cross the court chairman and take decisions based on the law; and the dependence of judges on officials within the judicial system is intensified”.

[DISCUSSION: “Bonds and barter in the sauna”, Financial Times, March 28, 2010].

Russia & its political culture. Writing about present-day Russia, Margareta Mommsen and Angelika Nussberger uncover the remnants of Stalinist political culture in matters related to the separation of powers and judicial independence. In the USSR, judicial independence was disdained as bourgeois prejudice. See their book Das System Putin. Gelenkte Demokratie und politische Justiz in Rußland (Beck, 2007) [details].

* * *

The Hermitage Capital story. In 2007, 230 million were stolen from Russian tax authorities by a gang of murderers who obtained “sham” judgments from judges in Moscow, St. Petersburg and Kazan. The fraud involved three subsidiaries of Hermitage that had paid taxes worth $230m. Soon after the police raid, these companies were fraudulently re-registered under new owners, who applied for, and immediately received, a tax rebate of $230m

[DOCUMENT: Hermitage Capital Video]

Lawyer Sergei Magnitsky found dead in his cell. Says Hermitage Capital’s Bill Browder: “Now, you have a bunch of law enforcement people who are essentially organised criminals with unlimited power to ruin lives, take property and do whatever they like and that's far worse than I have ever seen in Russia before. Russia is essentially a criminal state now.” From an unnamed senior banker in Mosow: “Russia's judicial system is totally compromised. It is strangling entrepreneurship. What happened is a clear impediment for investments coming in, not just for foreign investment but even for local ones”. (Catherine Belton: "Questions remain about Russia tax fraud", Financial Times). Note the point made by the senior banker: THE JUDICIAL SYSTEM STRANGLES ENTREPRENEURSHIP!!! Very much in line with Montesquieu-Smith.

[DOCUMENT: “Justice for Sergei”. See also The Economist: “Sergei Magnitsky one year on”, November 2010]

[QUESTION: WHAT CAN WE EXPECT FROM THOSE WHO SUPPLY LOANABLE RESOURCES IN THE RUSSIAN CREDIT MARKET]

On Russia’s “legal nihilism”. Olga Kudeshkina: “Tackling Russia’s Legal Nihilism”, OD Russia, 11 March 2010: “The powers of a judge who does not agree to carry out requests may be prematurely terminated. In such a situation the conscientious judge finds himself open to pressure from within the judicial system and has no chance of defending his or her own rights. As a result, fewer conscientious judges remain in service; their colleagues fear to cross the court chairman and take decisions based on the law; and the dependence of judges on officials within the judicial system is intensified”.

[DISCUSSION: “Bonds and barter in the sauna”, Financial Times, March 28, 2010].

Russia & its political culture. Writing about present-day Russia, Margareta Mommsen and Angelika Nussberger uncover the remnants of Stalinist political culture in matters related to the separation of powers and judicial independence. In the USSR, judicial independence was disdained as bourgeois prejudice. See their book Das System Putin. Gelenkte Demokratie und politische Justiz in Rußland (Beck, 2007) [details].

China

* * *

According to IMF data, China has a small local-currency bond market: only 28% of GDP. (Remember that bank credit plays a much larger role than bond financing in China).

Judicial independence in China (I). Randall Peerenboom specializes in China and the rule of law. He has just edited Judicial Independence in China. Lessons for Global Rule of Law Promotion (New York: Cambridge University Press, 2010 see). From the introduction:

This is the first book in English on judicial independence in China. This may not seem surprising given China remains an effectively single-party socialist authoritarian state, the widely reported prosecutions of political dissidents and the conventional wisdom that China has never had independent courts. On the other hand, this may seem surprising given that China has become a possible model for other developing countries – a model that challenges key assumptions of the multibillion-dollar rule of law promotion industry, including the central importance of judicial independence for all we hold near and dear. Although China's success in achieving economic growth and reducing poverty is well known, less well known is that China outscores the average country in its income class, including many democracies, on many rule of law and good governance indicators, as well as most major indicators of human rights and well-being, with the notable exception of civil and political rights. How has China managed all this without independent courts?

Judicial independence in China (II). An interesting case of Chinese innovation in the field of judicial independence. Liu Li: "Software helps judges mete out sentences", China Daily, July 9, 2006. It’s called computer-based sentencing!

[QUESTION: China is softening its stance on the death penalty by decreasing the number of offences that lead to it. Anything to do with … interest rates?]

China: Finance and the Judiciary. Patti Waldmeir: “Things improve, but judiciary still lacks independence”, Financial Times. Waldmeir quotes Australian lawyer Doug Clark: “The perception that the legal playing field is not level is a larger impediment to Shanghai's ambition to become a global financial centre by 2020 than any number of potholed streets or immature trading mechanisms. Without an independent legal system that resolves disputes fairly no one will bring real money to Shanghai. No one is going to park $1bn in Shanghai to pick up a bit of margin unless they have confidence that they can call a judge at 2am and get an injunction against behaviour that could damage them ... In a country without an independent judiciary, laws are only as good as the politicians allow them to be enforced”.

Ai Weiwei. David Piling: “Lunch with the FT: Ai Weiwei”, Financial Times, April 23, 2010. From one of his tweets: "No outdoor sports can be more elegant than throwing stones at autocracy; no melees can be more exciting than those in cyberspace". See his work at Haus der Kunst in Munich [see]; he also consulted with Swiss architects Herzog & de Meuron for the design of the Olympic Stadion in Beijing (The Nest). Says Ai Weiwei:

CHINA IS A COLOURFUL COUNTRY AND THERE IS A LOT OF FREEDOM. YET THE LACK OF AND INDEPENDENT JUDICIARY AND STATE LIMITS ON FREE SPEECH ARE FATAL FLAWS. CHINA IS LIKE A RUNNER SPRINTING VERY FAST BUT WITH A HEART CONDITION.

[DOCUMENT: “Who is afraid of Ai Weiwei?”]

See also Edward MacMillan-Scott: “Ai Weiwei's arrest is part of China's new crackdown”, The Guardian.

* * *

According to IMF data, China has a small local-currency bond market: only 28% of GDP. (Remember that bank credit plays a much larger role than bond financing in China).

Judicial independence in China (I). Randall Peerenboom specializes in China and the rule of law. He has just edited Judicial Independence in China. Lessons for Global Rule of Law Promotion (New York: Cambridge University Press, 2010 see). From the introduction:

This is the first book in English on judicial independence in China. This may not seem surprising given China remains an effectively single-party socialist authoritarian state, the widely reported prosecutions of political dissidents and the conventional wisdom that China has never had independent courts. On the other hand, this may seem surprising given that China has become a possible model for other developing countries – a model that challenges key assumptions of the multibillion-dollar rule of law promotion industry, including the central importance of judicial independence for all we hold near and dear. Although China's success in achieving economic growth and reducing poverty is well known, less well known is that China outscores the average country in its income class, including many democracies, on many rule of law and good governance indicators, as well as most major indicators of human rights and well-being, with the notable exception of civil and political rights. How has China managed all this without independent courts?

Judicial independence in China (II). An interesting case of Chinese innovation in the field of judicial independence. Liu Li: "Software helps judges mete out sentences", China Daily, July 9, 2006. It’s called computer-based sentencing!

[QUESTION: China is softening its stance on the death penalty by decreasing the number of offences that lead to it. Anything to do with … interest rates?]

China: Finance and the Judiciary. Patti Waldmeir: “Things improve, but judiciary still lacks independence”, Financial Times. Waldmeir quotes Australian lawyer Doug Clark: “The perception that the legal playing field is not level is a larger impediment to Shanghai's ambition to become a global financial centre by 2020 than any number of potholed streets or immature trading mechanisms. Without an independent legal system that resolves disputes fairly no one will bring real money to Shanghai. No one is going to park $1bn in Shanghai to pick up a bit of margin unless they have confidence that they can call a judge at 2am and get an injunction against behaviour that could damage them ... In a country without an independent judiciary, laws are only as good as the politicians allow them to be enforced”.

Ai Weiwei. David Piling: “Lunch with the FT: Ai Weiwei”, Financial Times, April 23, 2010. From one of his tweets: "No outdoor sports can be more elegant than throwing stones at autocracy; no melees can be more exciting than those in cyberspace". See his work at Haus der Kunst in Munich [see]; he also consulted with Swiss architects Herzog & de Meuron for the design of the Olympic Stadion in Beijing (The Nest). Says Ai Weiwei:

CHINA IS A COLOURFUL COUNTRY AND THERE IS A LOT OF FREEDOM. YET THE LACK OF AND INDEPENDENT JUDICIARY AND STATE LIMITS ON FREE SPEECH ARE FATAL FLAWS. CHINA IS LIKE A RUNNER SPRINTING VERY FAST BUT WITH A HEART CONDITION.

[DOCUMENT: “Who is afraid of Ai Weiwei?”]

See also Edward MacMillan-Scott: “Ai Weiwei's arrest is part of China's new crackdown”, The Guardian.

[ILLUSTRATION]. The Ambrogio Lorenzetti frescoes at Sienna (Palazzo Publico).

[1] Good government: equal justice, or the rule of law; [2] Good government: peace & prosperity in the city; [3] Peace, prosperity and SECURITY in the country side. [4] Tyranny: justice bound and gagged; [5] Tyranny: destruction inside the city; [6] Tyranny: the countryside.

{kind=link}

{kind=link}

{kind=link}

References. Chiara Frugoni: "Gli affreschi nel Palazzo Pubblico di Siena", in her book Pietro e Ambrogio Lorenz1etti (Milan: Scala, 1988); Hans-Jürgen Wagener: "Good governance, welfare, and transformation", The European Journal of Comparative Economics, junio 2004; Quentin Skinner: "Ambrogio Lorenzetti's Buon Governo frescoes: two old questions, two new answers", Journal of the Warburg and Courtauld Institutes, LXII, 1999.

French photographer Henri Cartier-Bresson is in Shanghai just a Maoist troops are about to take the city, in late 1948. (1, 2, 3). Note the anguish of depositors. They are rushing to take their money out of banks. Some of them are looking to the photographer.

[QUESTION: What do you think was happening to the supply of loanable resources at that very moment? Are interest rate going up or down? Why?

____________

Iran, 2010

[DISCUSSION: “Iranians switch to informal savings funds as loans dry up”, Financial Times, March 13, 2010].

______________________

Argentina, 2009

Another fascinating case. The country has an enormous wealth of natural resources; it is huge. Yet its per capital GDP is stagnant; poverty is widespread. What is going on? Here’s a hint. Argentina’s Supreme Court on criminalizing small amounts of drugs. Most recent rulings: 1978 (criminalizing); 1986 (de-criminalizing); 1991 (criminalizing); 2009 (decriminalizing). [Not required reading! Jonathan Miller: "Judicial Review and Constitutional Stability: A Sociology of the U.S. Model and Its Collapse in Argentina", Hastings International and Comparative Law Journal, Vol. 77, No. 21, 1997].

In other words, the Argentine Supreme Court does not follow its own precedents!

Argentina: the concept of “strategic defection”, developed by Gretchen Helmke. Courts under Constraints. Judges, Generals, and Presidents in Argentina (New York: Cambridge University Press, 2005) [webpage] [see] [review].

________________________

England, 1300 (Braveheart)

In 1300, king Edward I is at war with the Scots. He needs lots of money. There is no tax system as we understand it today. The barons and the London merchants are unwilling to assist the king with more funds, unless he re-issues Magna Carta. "When we have secure possession of our forests, and of our liberties, often promised to us, then we will willingly give a twentieth, so that the folly of the Scots may be dealt with" (p. 525). Very interesting! It pays to strengthen the rule of law! Meanwhile, Edward puts tremendous pressure on courts to expropriate as much resources as possible. There is little information about the level of interest rates at that time, because lending at interest was forbidden by the Church. However, we learn that an investigation of Jewish bankers yields a very interesting discovery: many loans carry a 43% interest rate! (*)

(*) Michael Prestwich. Edward I (University of California Press, 1988).

___________________________

Europe & Precedents as a source of law

- The Netherlands: “There is no stare decisis in Dutch law, as there is in common law [mostly English-speaking countries], although in practice the Supreme Court will not usually overrule its own previous decisions” (Sanne Taekama, ed. Understanding Dutch Law. Boon Juridische uitgevers, 2004).

- The European Court of Justice: “Where a question referred to the Court for a preliminary ruling is identical to a question on which the Court has already ruled, where the answer to such question may be clearly deduced from existing case-law or where the answer to the question admits of no reasonable doubt, the Court may, after informing the court or tribunal which referred the question to it, give its decision by reasoned order in which, if appropriate, reference is made to its previous judgment or to the relevant case-law” (Hans Baade: “Stare Decisis in Civil Rights Countries: The Last Bastion”, in Peter Birks & Adrianna Pretto, eds. Themes in Comparative Law. In Honor of Bernard Rudden. Oxford: Oxford University Press, 2002);

- Finland Supreme Court (see): “The most important function of the Supreme Court is to establish judicial precedents in leading cases thus ensuring uniformity in the administration of justice by the lower courts”.

- Sweden Supreme Court (see): “Leave to appeal is required for a case to be considered. This is granted by the Supreme Court itself, basically only in those cases where it is important to establish a judgment that may provide guidance for the Swedish district courts and courts of appeal. Such judgments are called precedents”.

__________________

More stories

- Venezuela & “onerous financing costs”. Oil development in the Orinoco Belt is in jeopardy: “Repeated delays in the bidding for rights to exploit the Orinoco Belt reflect investor concerns about political risk, onerous financing costs and the profitability of the projects” (Benedict Mander: “Chávez a problem for oil groups eyeing vast field”, Financial Times). Note that both Venezuela and Iran are usually the most aggressive OPEC member countries when it comes to reduce output …

- Tunisia. Thomas Fuller: “Head of Reform Panel Says Tunisia Risks Anarchy as It Moves Toward Democracy”, The New York Times. Abdelrazek Kilani, president of the Tunisian Bar Association, estimated that “about 100 judges are totally corrupt” and needed to be removed. ‘They took bribes and followed orders from the Ministry of Justice,’ Mr. Kilani said in an interview. ‘They convicted people because the ministry told them to’. The country’s official unemployment rate is 14 percent, concentrated among young people, but the rate is much higher in Sidi Bouzid, say local union leaders, who put it at higher than 30 percent. Neglected by successive central governments, bereft of factories, seized with corruption and rife with nepotism, Sidi Bouzid and the small towns surrounding it are filled with idle young men, jobless, underemployed or just plain poor.

- From an IMF study. John D. Burger & Francis E. Warnock: “Local Currency Bond Markets”, IMF Staff Papers, Vol. 53, 2006 (only pp. 141-142). “The importance of institutional and policy settings suggests that even emerging economies have the ability to develop local currency bond markets. Emerging market economies are not predestined to suffer from original sin. To gauge the importance of various factors, our estimates in column 1 of Table 3 imply that (other things being equal) if Brazil had Denmark’s rule of law, its bond market as a share of GDP would be 43 percentage points higher. If Brazil had Denmark’s inflation history, its bond market would be 42 percentage points (of GDP) larger. These amounts are both economically significant—Brazil’s local currency bond market is currently only 22 percent of GDP—and suggest an important role for creditor-friendly policies in emerging markets. The results suggest that the determinants of the size of government and private bond markets are quite similar: Countries with better inflation performance and stronger rule of law have larger sovereign and corporate bond markets”. [MY COMMENT: Think about it! Brazil’s GDP is about $1.27 trillion. Now, 43 percentage points would mean that no less than $546 billion that could be made available to entrepreneurs and/or to the government (poverty reduction, etc)].

- Singapore. Lee Kwan Yew: Keynote speech , International Bar Association Conference, Singapore, October 14 2007: “Important for investors and economic growth is the rule of law, implemented through an independent judiciary, an honest and efficient police force, and effective law enforcement agencies. The rule of law would give Singapore an advantage in Southeast Asia where the law was often what was decided by the leader. A stable and predictable legal environment facilitates the enforcement of contractual rights and protection of property rights. The independence of our courts is protected by the constitution that prevents removal of judges by the executive. We still look to English precedents and examples, but increasingly we look as well to those of the US, Australia, New Zealand. This also needed a Chief Justice who is not only legally qualified, but also has managerial and administrative experience to reform the system. [We] selected the most able and balanced of those at the Bar to become judges. Good governance, a sound legal framework and judiciary have resulted in stability and economic growth”.

- United States. In most American states, local judges are elected by the people. According to The New York Times: “As spending in state judicial races by special interests has vastly escalated in recent years, so has the threat to public confidence in judicial neutrality that is fundamental to the justice system”. [New York Times: "Fair Courts in the Cross-Fire"].

- Nigeria. A BBC documentary highlights the case of a talented Lagos entrepreneur (in the gas station business) whose main complaint is the high cost of capital: 25%! By definition, credit depends on confidence and —as Adam Smith put if— on the performance of contracts. Can we trust the performance of contracts when we see scenes like this one?

_____________

Monday, April 4, 2011

From the website of the Dubai International Financial Centre:

“Perhaps now is the opportunity for Islamic Finance to come out from the shadows of conventional finance and provide financial products in line with Shariah to an investor base that is currently unsatisfied and unsure of the conventional financial system,” said Abdulla Al Awar, Chief Executive Officer of DIFC Authority.

There are many factors for this phenomenon. Many conventional forms of banking and insurance have been prohibited or restricted in the Islamic World on the grounds that they contravene the tenets of Islam. But, in recent years, there has been a dramatic growth in Islamic or Shariah-compliant financial products, reflecting a number of trends including changes in Islamic law such as the approval in 1985 by the Grand Counsel of Islamic scholars of the Takaful system as the alternative form of insurance written in compliance with Islamic Shariah and the emergence of an international market in Sukuk (Shariah-compliant) bonds.

Other factors are economic development giving rise to infrastructure and other projects which require Shariah-compliant forms of financing, rising incomes among the Arab population resulting in the need for Islamic consumer financial products such as insurance, mortgages, pension plans and investment funds, and changing demographics resulting in the growing need for pensions and other retirement savings products.

The publication points out that the total size of the Islamic Banking industry is currently estimated to be between US $800 billion to $1trillion, and is estimated to have a global potential of $4 trillion. It is growing at 15-20 per cent per annum and within the next 8-10 years Islamic banking industry is projected to capture half of the savings of the world’s 1.6 billion Muslims.

Currently, market penetration amounts to an estimated 20 per cent of the Arab population. This figure is expected to rise dramatically and it is expected that within the next decade, 50 to 60 per cent of the total savings of the world's 1.2 billion Muslims will be in the form of Shariah compliant products.

More interestingly, as conventional banking faces troubled times, Islamic banking, which is asset-backed as opposed to debt-based, offers a viable alternative and is becoming increasingly popular in global financial capitals such as London, which ranks second after Dubai in terms of the number of listed sukuks.

The publication says assets under management in Islamic Funds are estimated to be between $50-70 billion and the total value of sukuks issued is valued at more than $88 billion, of which $13 billion is listed on NADAQ Dubai.

[QUESTIONS: Is $88 billion a significant figure? Who are Dubai's key competitors in Islamic finance?]

* * *

In a speech at the 5th World Islamic Economic Forum in Jakarta, on 2 March 2009, president Yudhoyono mentioned the C-Word [see]:

Indonesia is honored to be the host of this year’s World Islamic Economic Forum. I have always been supportive of this Forum, both as a progressive muslim and as patron of the WIEF national committee. I have always believed that what we seek to achieve through the WIEF is more than just economic cooperation. What we aspire is to promote greater friendship, brotherhood and solidarity among muslims, and between nations. We want to see the ummah becoming enlightened and empowered to address 21st century challenges. For the the 21st century will be an era unlike any other era before. The 20th century was known as the century of hard power; the 21st century we hope is the century of soft power. The 21st century will be driven by openness, technology, connectivity, dialog, and integration. It will be the age of possibility and opportunity. That is why the WIEF is relevant because it helps the ummah adapt to that wondrous world. The ummah can shape and have full ownership of the 21st century. But first we must make the ummah a stake-holder, and we must empower them. The ummah can once again become a key driver of globalization, just the way we were the world’s first globalizers in the 13th century. Only by embracing excellence and innovation, can the ummah, after centuries of marginalization, make that great leap forward in this amazing century. Let us begin now.

Assignment No. 2 – April 14, 2011

Session 2 - April 7

Find at least one modern example for each of the five types of Schumpeterian innovation (500-word essay). Please cite your sources: books, journals, newspapers, company website, website, etc. Please cite (only if available) statistics of market size. Be sure to mention innovations, not just inventions. If you think that an invention does have the potential to become an innovation, briefly state the business case!

[REQUIRED READING!] Excerpt from Joseph A. Schumpeter. The Theory of Economic Development, as quoted by Thomas McCraw in Prophet of Innovation. Joseph Schumpeter and Creative Destruction (Cambridge, Massachusetts: Harvard University Press, 2007):

Schumpeter specifies five types of innovation that define the entrepreneurial act. To quote his list directly:

(1) The introduction of a new good –that is one with which consumer are not yet familiar- or of a new quality of a good.

(2) The introduction of a new method of production [or commercialization], that is one not yet tested by experience in the branch of manufacture [or retail trade] concerned.

(3) The opening of a new market, that is a market into which the particular branch of manufacture of the country in question has not previously entered, whether or not this market has existed before.

(4) The conquest of a new source of supply of raw materials or half-manufactured goods, again irrespective of whether this source already exists or whether it has first to be created.

(5) The carrying out of the organization of any industry, like the creation of a monopoly position, or the breaking up of [an existing] monopoly position.

_____________

Session 2 - April 7

Find at least one modern example for each of the five types of Schumpeterian innovation (500-word essay). Please cite your sources: books, journals, newspapers, company website, website, etc. Please cite (only if available) statistics of market size. Be sure to mention innovations, not just inventions. If you think that an invention does have the potential to become an innovation, briefly state the business case!

[REQUIRED READING!] Excerpt from Joseph A. Schumpeter. The Theory of Economic Development, as quoted by Thomas McCraw in Prophet of Innovation. Joseph Schumpeter and Creative Destruction (Cambridge, Massachusetts: Harvard University Press, 2007):

Schumpeter specifies five types of innovation that define the entrepreneurial act. To quote his list directly:

(1) The introduction of a new good –that is one with which consumer are not yet familiar- or of a new quality of a good.

(2) The introduction of a new method of production [or commercialization], that is one not yet tested by experience in the branch of manufacture [or retail trade] concerned.

(3) The opening of a new market, that is a market into which the particular branch of manufacture of the country in question has not previously entered, whether or not this market has existed before.

(4) The conquest of a new source of supply of raw materials or half-manufactured goods, again irrespective of whether this source already exists or whether it has first to be created.

(5) The carrying out of the organization of any industry, like the creation of a monopoly position, or the breaking up of [an existing] monopoly position.

_____________

Session 2, April 7 2011

Now this is an exciting topic! Joseph A. Schumpeter (1883-1950) is the key pioneer in the field of economics and innovation. Schumpeter wrote the Theory of Economic Development in 1911, almost 100 years ago! Schumpeter on the credit market: “He can only become an entrepreneur by previously becoming a debtor … what he first wants is credit. The core ethos of capitalism looks constantly ahead and relies on credit in launching new ventures. From the Latin root credo —'I believe'— credit represents a wager on a better future ... In the absence of credit, both consumers and entrepreneurs would suffer endless frustrations”.

Initially, the emergence of innovative entrepreneurs pushes interest rates higher, as demand for credit shifts upward.

[DIAGRAM. Demand for credit increases at each level of the interest rate!]. The result is a higher level of interest rates…

Now, Schumpeter also praised financial innovation — up to a point. In the case of railroads in the second half of the XIXth century, or the automobile industry, he states that “credit creation” in the form of overdrafts and car loans [i.e credit creation on a large scale] made it possible to finance these innovations.

[DIAGRAM. The supply of loanable resources increase]. Note that the net result is a stable interest rate + more credit!!! This is the kind of result you want to have!

But then he adds: “Some of that lending was granted with almost unbelievable freedom and carelessness”. Does that ring a bell? Sounds familiar? BOOM-AND-BUST IS INDEED PART OF THE PACKAGE!!!!. Schumpeter made a distinction between productive & non-productive financial instruments. When bankers create financial instruments to “play amongst themselves”, then the risk of a bubble increases dramatically. But is it possible to really make that distinction? On this topic, see [NOT required reading!] the paper by Charles G. Leathers & J. Patrick Raines: “The Schumpeterian role of financial innovations in the New Economy's business cycle” Cambridge Journal of Economics, 2004, No. 28, Vol. 5, pp. 667-681.

_____________

Innovation vs. invention

An innovation is an invention with a proven track record in the market place! Please remember this point when writing Assignment No. 2!

______________

Leiden University 2011 - Agustin Mackinlay (mackinlaya@fsw.leidenuniv.nl)

Session 2. April 7, 2011

____________________

An Introduction to Credit Markets

The importance of interest rates

Credit, it has been said, is the lifeblood of the modern economy. The capital resources available to entrepreneurs (and therefore job creation), the cost of the public debt (and therefore future tax levels), the value of our homes — all depend on the availability of credit and on the level of interest rates.

Credit is power! In his biography of the Duke of Marlborough, Winston Churchill marvels at the power of the City of London to “manufacture” credit and win the war against Louis XIV. See also Gideon Rachman’s recent book: the 2008 financial crisis will be remembered as the moment when the US finally lost its position as the only global superpower.

Emerginmg powers across the world are taking steps to beef up their financial systems and credit markets in order to provide households, entrepreneurs (and goivernments) with reliable credit instruments. (See DIFC, HKMA).

With that in mind, one remembers US Democratic strategist James Carville famously quipping that he wanted to be “reincarnated as the credit [bond] market because it can intimidate everybody”.

Credit & wage levels. Countries that face a high cost of labor and —simultaneously— high interest rates (cost of capital) usually are in deep trouble: Argentina 1999-2001, Greece 2010. Such situations usually will require new solutions in terms of financial diplomacy.

Long –term interest rates and the Horace Brock Paper

[QUESTION: Who sets interest rates?]

Journalists would have us believe that central banks set interest rates. This is true with respect to short-term interest rates: central banks have a number of instruments at their disposal to set the interest rate at which commercial bank lend to themselves for very short periods of time (usually overnight).

But you don’t build a factory, you don’t buy yourselves a home on an overnight loan!

That’s where the excellent Horace Brock paper comes in. Long-term interest rates (10 years or more) are set on the largely deregulated and globalized credit market. The key merit of the Brock paper is that it provides us with a very simple framework to understand how long-term interest rates are set. It is a plain supply and demand framework, much as if we would be analyzing the supply and demand for apples or oranges. True, the paper has aged a bit, but we can update it pretty easily.

[REQUIRED READING! Horace Brock: "Determinants of interest rates", in Boris Antl (ed.). Management of Interest Rate Risk (London: Euromoney Publications, 1988].

An ‘extended’ law of supply and demand

How do we analyze the determinants of interest rate movements in today’s deregulated, globalized environment? What paradigm is most appropriate? We shall argue that the complexities of today’s environment require that we analyze interest movements in what can be called an ‘extended’ law of supply and demand in the credit market. Although this approach is both theoretically correct and intuitively appealing, it is surprisingly unfamiliar to market participants as well as to many who construct forecasting models.

Surprisingly, one reason this is true is that most people do not understand what the law of supply and demand means in a credit (as opposed to a money) market context. In this regard, shifts in credit supply and demand are often mistakenly identified with changes in economic flow-of-funds. In other instances, supply and demand considerations are incorrectly seen as incompatible with more important ‘psychological’ factors. This chapter will clarify the true meaning of supply and demand in today’s deregulated credit market. In doing so, it will demonstrate how the extended law of supply and demand is able uniquely to explain numerous dramatic events in credit markets.

The extended law of credit supply and demand Exhibit 1 [not reproduced here] shows the working of today’s credit market. On the left are those who ‘lend’. Note that the central bank fits in here in a natural way via its open market activities that provide bank reserves to the banking system. As the diagram indicates, it is the banks that provide credit — not the central bank.

How do interest rates change within this framework? They change when the behavior of borrowers and lenders/investors changes. But what do we mean by a ‘change of behavior’? Understanding this concept is the key to everything. The ‘supply schedule’ here can be best thought of as the nation’s aggregate ‘willingness to lend’ schedule (foreign lending is included). This schedule depicts the total amount of funds that will be made available at any given nominal interest rate. Naturally, the higher the interest rate, the more credit will be made available, other things being equal. Hence the schedule has a positive slope. A parallel analysis holds for the demand schedule, although in this case the quantity demanded decreases as the price rises. Equilibrium occurs at the point of intersection of the two schedules.

Changes in interest rates

As the state of the world changes, the aggregate willingness to lend at any given interest rate (say € 500bn annually at a 5% interest rate) will change. It will either increase or decrease. For example, if inflation escalates, people might only be willing to lend € 400bn at the same 5% nominal rate. But as this decrease will be true for any and every level of interest rates, the entire schedule clearly shifts backward. It is this ‘functional shift’ (of the schedule) that causes interest rates to change.+

Why do we emphasize this point? Because it is often misunderstood. For example, suppose you hear that ‘mortgage credit demand has increased’. Does this constitute a ‘change’ that will lead to an increase in interest rates? Not necessarily. If the increased demand is itself simply a response to a lower interest rates, then this increase represents a shift ‘along’ the given demand curve. It is only when demand is greater or lesser at a given interest rate that the entire schedule shifts, and this that interest rates can and do change.

[END OF THE HORACE BROCK PAPER]

___________________

Bank Credit and Bond Markets

Roughly speaking, there are two broad credit channels. Bank credit: depositors entrust their assets to commercial banks, who in turn loan out those resources. Banks make a profit from the difference between the rates they charge to their clients and the rates they pay on deposits. By lending out money to households, entrepreneurs and corporations, banks take on credit risk. It is a highly regulated industry; banks need to hold capital against the contingency of loan defaults!

A bond is a contractual obligation that is performed directly between borrowers and lenders, that is, without the intermediation of banks. A bond specifies the amount of the loan, its maturity, its interest rate. Bond markets have reached a very high degree of sophistication in most English-speaking countries.

Sunday, April 3, 2011

iRevolutions or Net Delusion?

* * *

[VIDEO: "Diplomacy in a Digital World", by Alec Ross, Senior advisor for innovation to US Secretary of State Hillary Clinton]

Cyber-Realists: (1) Evgeny Morozov. The Net Delusion. How Not to Liberate the World (New York: Allen Lane, 2010) [Twitter]; (2) Rebecca McKinnon: “Global Internet Freedon and the Rule of Law, II”. [Blog].

* * *

[VIDEO: "Diplomacy in a Digital World", by Alec Ross, Senior advisor for innovation to US Secretary of State Hillary Clinton]

Cyber-Realists: (1) Evgeny Morozov. The Net Delusion. How Not to Liberate the World (New York: Allen Lane, 2010) [Twitter]; (2) Rebecca McKinnon: “Global Internet Freedon and the Rule of Law, II”. [Blog].

Tom Friedman: Food Prices & Revolutions (On Economic Connectivity)

* * *

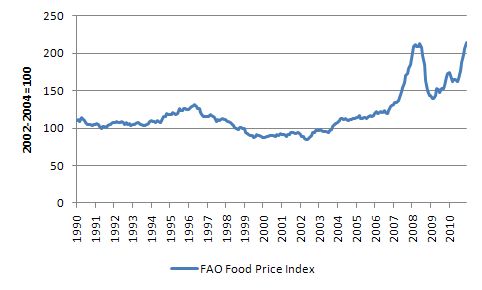

A key element of the Revolutions in Tunisia and Egypt: rising food prices. As food and energy prices rise and public budgets come under strain, some food and gas subsidies are eliminated — thus creating the conditions for mass protests. But what is the ultimate cause of those food price increases? The short answer: China’s connection to the world economy.

See Thomas Friedman: “China, Twitter and 20-Year-Olds vs. the Pyramids”, The New York Times: “Of course, China per se is not fueling the revolt here — but China and the whole Asian-led developing world’s rising consumption of meat, corn, sugar, wheat and oil certainly is. The rise in food and gasoline prices that slammed into this region in the last six months clearly sharpened discontent with the illegitimate regimes — particularly among the young, poor and unemployed”. [DATA: Wheat prices chart; oil prices chart]

See Thomas Friedman: “China, Twitter and 20-Year-Olds vs. the Pyramids”, The New York Times: “Of course, China per se is not fueling the revolt here — but China and the whole Asian-led developing world’s rising consumption of meat, corn, sugar, wheat and oil certainly is. The rise in food and gasoline prices that slammed into this region in the last six months clearly sharpened discontent with the illegitimate regimes — particularly among the young, poor and unemployed”. [DATA: Wheat prices chart; oil prices chart]

* * *

A key element of the Revolutions in Tunisia and Egypt: rising food prices. As food and energy prices rise and public budgets come under strain, some food and gas subsidies are eliminated — thus creating the conditions for mass protests. But what is the ultimate cause of those food price increases? The short answer: China’s connection to the world economy.

* * *

Not an abstract discussion! What seemed exceedingly abstract only a few days ago has now become a very tangilbe matter: what to do about Libya? What to do about Bahrain, Syria? Every one of the so-called Great Powers ––America, Canada, the EU, BRICs–– has to take a stance on Libya. It’s a battle between realists and liberals! Read the following statements and analyze whether they come from a LIBERAL o REALIST perspective. In each case, briefly state the opposing argument. Most answers are obvious; but the point of this discussion is to remember that great powers sometime have to take dramatic decisions in a matter of … days.

Background info: Libya and oil. Map of oil and gas resources. Before the crisis, Libya produced 1.58 million barrels of oil per day, about 2% of global oil supplies. Oil price rose sharply [chart]. However, Opec’s spare capacity stands at about 4.7m b/d — a comfortable cushion. A contagion scenario affecting production in Algeria, Oman, Yemen and Bahrain would see prices skyrocket to about $150-$220/barrel. Were unrest to hit Saudi Arabia, the spike could be sharper. And that would mean a very sharp worldwide recession.

{kind=link}

[1] “If Col Gaddafi’s regime wins its civil war, consider the next phase. There will be more massacres and refugees. What then? Indefinite containment and sanctions on a pariah state endowed with wealth, pathological leadership and experience in state use of clandestine terror networks An objective can be stated simply: Col Gaddafi out of power”. (Philip Zelikow: “Only a no-drive zone can stop Gaddafi’s forces now”, Financial Times, March 26). Counsellor of the US Department of State, 2005-2007.

[2] “Absolute monarchies in the Arab world will need to contemplate constitutional monarchy and power sharing of they are to survive” (David Gardner: “And so to chapter two of the great Arab awakening”, Financial Times, March 20).

[3] “America has little strategic interest in north Africa but a lot at stake in the Gulf”. (Quoted by David Gardner: “And so to chapter two of the great Arab awakening”, Financial Times, March 20).

[4] “Hosni Mubarak kept conflicts at bay; authoritarian regimes in the region are the only alternative to chaos or radical Islam”. (Quoted by Roula Khalaf: “Making history in the street”, Financial Times, March 27).

[5] “In the region, 60% of the population is under 25; they have the internet, and they are aware of the things that happen around the world”. (Quoted by Roula Khalaf: “Making history in the street”, Financial Times, March 27).

[6] “Mohamed El-Baradei, Nobel laureate and opposition figure: they [the networked generation] know that nothing will change in terms of social justice and economic demands except through democracy”. (Quoted by Roula Khalaf: “Making history in the street”, Financial Times, March 27). [ElBaradei video].

[7] “Western powers are nervous about being sucked into a third war in an Islamic country after the painful experiences of Afghanistan and Iraq”. (Quoted by David Gardner: “And so to chapter two of the great Arab awakening”, Financial Times, March 20).

[8] “Mr Cameron is plainly guided by moral conviction; but this is a dangerous indulgence for a leader facing so many problems at home”. (Max Hastings: “Why the military is right to fret over Libya”, Financial Times, March 25).

[9] “Should this commitment expand any longer in terms of cost, time or intensity, I do think it’s important for Congress to be consulted and included in the decision-making process”. (Senator Chris Coons, a Democrat member of the Senate foreign relations committee, quoted by Richard McGregor: “Obama struggles for clarity in messy conflict”, Financial Times, March 25).

[10] “The main matter in the Middle East: managing Egypt’s democratic transition, and the Gulf, where a crackdown on Bahrain threatens to exacerbate Shia-Sunni tensions”. (Richard McGregor: “Obama struggles for clarity in messy conflict”, Financial Times, March 25).

[11] “We cannot be sure whether what we are seeing is a genuine democratic revolution; repression could rule the day. Anarchy, civil war, harsh police states, sectarianism, and severe Islamic rule are all potential alternatives to the sort of authoritarian regimes that have recently dominated the region. All of those outcomes are possible; none is likely to lead to greater freedom. Overall, we must be realistic about what to expect from a small degree of democratization. Immature or partial democracies are vulnerable to being hijacked by populists or extreme nationalists. A Middle East more influenced by public opinion could well be less willing to work against terrorism, or on behalf of peace with Israel. It is likely to be no more of a partner when it comes to providing oil at reasonable prices”. (Richard Haass: “How to read the second Arab awakening”, Financial Times, March 9). [video]. President, Council on Foreign Relations.

[12] “The Syria/Iran/Hizballah axis is a huge benefit to Iran and ending it would weaken Iran’s position greatly. Syria is Iran’s only ally in the Arab world and its land bridge to Hizballah. Recent reports of an Iranian naval facility in the Mediterranean reminded us of how valuable an asset Syria is today for Iran. If a Sunni-led Syria (and the country is 74% Sunni) ended the Asad regime’s romance with the ayatollahs, American interests in the entire Middle East would gain. Hizballah’s power in Lebanon would diminish instantly and the opposition to Hizballah—the March 14 movement, and Lebanon’s Sunni, Christian, and Druze communities—would grow stronger. Iran’s ability to threaten Israel would diminish if it lost what amounts to a land border with Israel through Lebanon’s Hizballah-controlled south. Moreover, every time a Middle Eastern tyranny falls, and especially so in the case of the tyranny most closely linked to Iran, it makes Iran’s own terrorist regime seem more outdated and anomalous in a Middle East where democracy is spreading.” (Elliott Abrams: “Syria, Iran, and American Interests”, Council on Foreign Relations, March 26).

[13] “For Moscow, the unrest in the Arab world is oddly double-edged. The resulting spike in oil prices has boosted Russia’s economy. On the face of it, the turmoil is a boon for Russia’s resource-dependent economy, taking oil prices close to the $120 a barrel in recent weeks. Economists say the increased prices could lift economic growth by 1 percentage point this year to at least 5%, the highest since 2008. Alexei Kudrin, finance minister, said in Monday that Russia’s budget deficit —built up through heavy spending during the financial crisis— would be eradicated if oil averaged $115 this year. Every $10 increase in the average price of crude oil swells Russia’s revenues by $20bn. That calculus underlie Moscow’s decision to abstain at the UN Security Council on Resolution 1973. Yet the Kremlin is watching uneasily the Middle East backlash against authoritarianism, corrupt and wealthy leaderships. ‘There is a sort of nervousness here that no one has observed before’, said an experienced foreign banker. ‘People are worried about contagion’. The oil windfall could restore Russia’s pre-crisis complacency, tempting it to backtrack on much needed corruption and reducing the state’s role in the economy. Polls suggest support for President Medvedev and Vladimir Putin, prime minister, remains at about 70%. But there have been signs of official jitters. (Catherine Bolton & Neil Buckley: “Russia in dilemma on Arab unrest”, Financial Times, March 16).

[14] “On Monday, officials were confronted with a rare moment of open disagreement between the two men who run the country. Prime Minister Vladimir V. Putin issued a lacerating critique of the allied attacks on Libya — the kind of protest that accompanied Western interventions in Iraq and Kosovo. President Dmitri A. Medvedev, who had articulated a more pro-Western position, rebuked his mentor, calling Mr. Putin’s language unacceptable.” Ellen Barry: “Leaders’ Spat Tests Skills of Survival in the Kremlin”, The New York Times, March 2011.

Liberal: Thomas Barnett

Liberal: Thomas Barnett. Thomas P.M. Barnett: Twitter; blog; video; The Pentagon’s New Map. War and Piece in the XXIst. Century (New York: Putnam, 2004) [webpage].